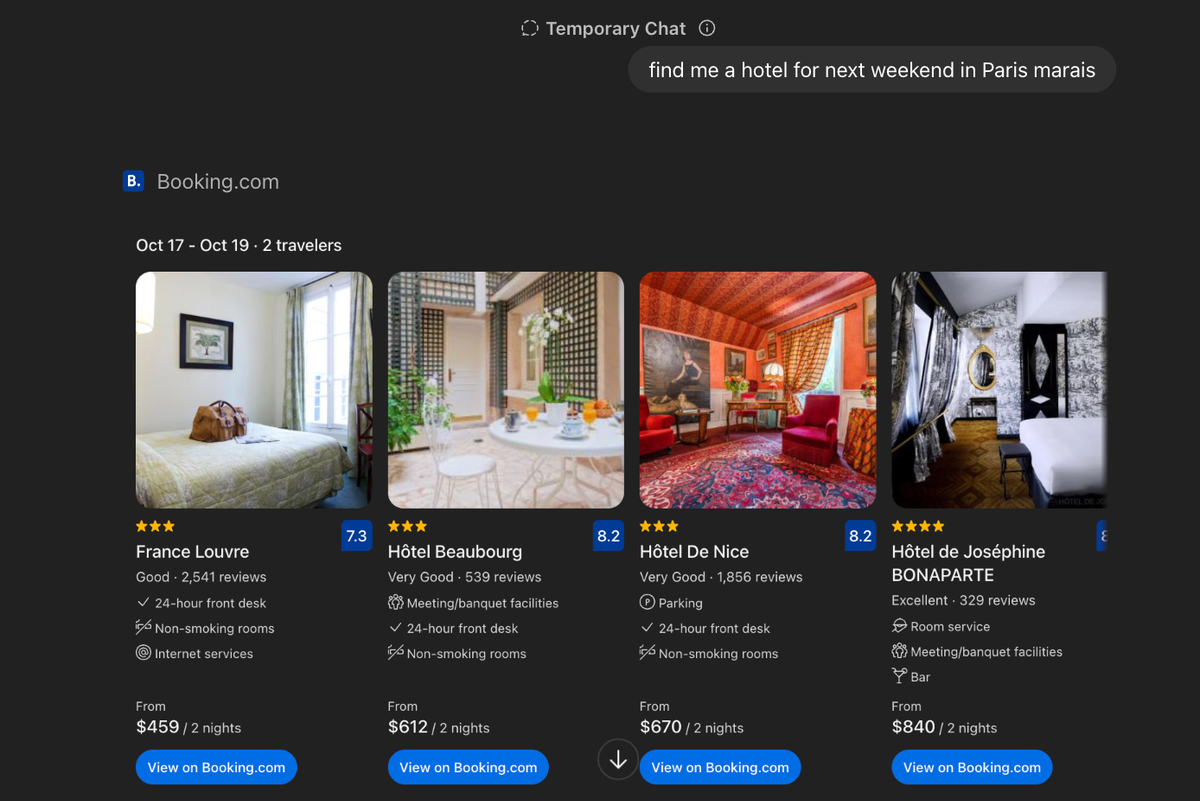

OTAs are now integrated into ChatGPT

OpenAI is bringing apps inside ChatGPT — interactive interfaces directly within the chat, starting with partners like Booking.com, Expedia, and soon TripAdvisor (with many more to come).

AI and SEO expert at the forefront of AI Search. He analyses models daily and runs hospitality-focused experiments on a database of over 1M prompts, citations and mentions.

ChatGPT is becoming a distribution channel. OTAs like Booking and Expedia will be able to integrate directly into the chat.

Mechanically, this should increase the OTA share — and therefore reduce margins. We’re trying to decode the first effects.

A new frontier: app suggestion

OpenAI has opened apps inside ChatGPT. In practice, this means two things:

You can now connect directly to Booking.com or Expedia through the interface.

More interestingly, for “relevant” queries, ChatGPT can automatically connect to OTAs to display hotels.

I think this second part is the crucial one. With a limited interface (that of ChatGPT), it raises major questions about suggestions, sources (even if you pick an OTA — which one, or which ones?), and the overall user journey.

Given the likely opening to all apps — and therefore all OTAs — the only viable way to prioritize results will inevitably be… sponsorship.

Ranking & User Interface (UI): same thing — just worse?

Inside an app, the ranking follows that app’s own system. Naturally, Booking.com’s ranking — which is based on many factors, including sponsorship — will likely be the same as on its website… but displayed within a much more limited interface.

Indeed, ChatGPT’s interface is inherently more “minimal” within the chat:

- Fewer results. For now, only a few listings appear — not full pages of options.

- Fewer native filters. Combining multiple filters will always be more cumbersome through a chat interface.

- Less space. Simply a different user experience.

With the launch of Atlas, ChatGPT’s web browser, this could change slightly — but at that point, you’d already be on Booking’s website while still being connected to Booking through ChatGPT.

Strange dynamic, to say the least.

What impact on direct bookings vs. OTAs?

As I mentioned earlier, there will be two streams: the upstream connection (where users link their account) and the in-app call.

For now, we haven’t seen a major difference — a slight drop in direct bookings on the faster models, but not really on the base model.

Direct Links vs OTAs per GPT-5 model (%)

With what business model ($$$)?

There’s a kind of mix here between Apple’s App Store and Google’s search model.

🔵 Blue Pill → A Google-like model: organic and sponsored results within chats, monetized by cost-per-click.

⚪️ Grey Pill → An Apple-like model: the user chooses their “preferred” app early in the conversation, monetized through revenue sharing.

🔴 Red Pill → A completely new model? Yet to be invented…

And what about the user in all this?

When Sam Altman announced the arrival of apps, he emphasized a user-centric approach.

But if, in the long run, only one or a few OTAs are being pushed, we lose two fundamental elements:

- The power of the LLM itself — unbiased and unsponsored.

What’s the point if we just end up seeing the same ranking as on Booking.com… paid for by hotels?

- Trust.

If users keep receiving the same OTA suggestions, it’s hard to imagine they’ll remain confident — or satisfied.

They’d likely go directly to the OTA or pre-activate the app instead.

Measurement will remain essential.

Whatever the model, just as we have ASO (App Store Optimization) and SEO (Search Engine Optimization) today, I believe there will always be some form of AEO / GEO — or whatever name eventually sticks.

And since there are still no clear statistics, it will be crucial to know whether an app is being suggested, featured, or not shown at all within a conversation.

Outside the EU (for now)

Apps are currently available outside the EU, with Europe announced as “coming later.”

It remains to be seen how long this gap will last.

Questions for the future

- How can 100 OTAs coexist within a single app?

- The “store” logic always creates a hierarchy — some will be visible, others invisible.

- Will there be sponsorships?

- If visibility becomes scarce, it will inevitably be monetized. The question is no longer if, but how.

- How will intermediary margin costs be passed along?

- Between commissions, sponsored placements, and paid integrations, the economic equation is bound to evolve.

- And what about voice?

- Voice integration could change everything — when there’s only one audible answer, the battle for the zero position becomes existential.